Mean Reversion Pro Strategy [tradeviZion]Mean Reversion Pro Strategy : User Guide

A mean reversion trading strategy for daily timeframe trading.

Introduction

Mean Reversion Pro Strategy is a technical trading system that operates on the daily timeframe. The strategy uses a dual Simple Moving Average (SMA) system combined with price range analysis to identify potential trading opportunities. It can be used on major indices and other markets with sufficient liquidity.

The strategy includes:

Trading System

Fast SMA for entry/exit points (5, 10, 15, 20 periods)

Slow SMA for trend reference (100, 200 periods)

Price range analysis (20% threshold)

Position management rules

Visual Elements

Gradient color indicators

Three themes (Dark/Light/Custom)

ATR-based visuals

Signal zones

Status Table

Current position information

Basic performance metrics

Strategy parameters

Optional messages

📊 Strategy Settings

Main Settings

Trading Mode

Options: Long Only, Short Only, Both

Default: Long Only

Position Size: 10% of equity

Starting Capital: $20,000

Moving Averages

Fast SMA: 5, 10, 15, or 20 periods

Slow SMA: 100 or 200 periods

Default: Fast=5, Slow=100

🎯 Entry and Exit Rules

Long Entry Conditions

All conditions must be met:

Price below Fast SMA

Price below 20% of current bar's range

Price above Slow SMA

No existing position

Short Entry Conditions

All conditions must be met:

Price above Fast SMA

Price above 80% of current bar's range

Price below Slow SMA

No existing position

Exit Rules

Long Positions

Exit when price crosses above Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

Short Positions

Exit when price crosses below Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

💼 Risk Management

Position Sizing

Default: 10% of equity per trade

Initial capital: $20,000

Commission: 0.01%

Slippage: 2 points

Maximum one position at a time

Risk Control

Use daily timeframe only

Avoid trading during major news events

Consider market conditions

Monitor overall exposure

📊 Performance Dashboard

The strategy includes a comprehensive status table displaying:

Strategy Parameters

Current SMA settings

Trading direction

Fast/Slow SMA ratio

Current Status

Active position (Flat/Long/Short)

Current price with color coding

Position status indicators

Performance Metrics

Net Profit (USD and %)

Win Rate with color grading

Profit Factor with thresholds

Maximum Drawdown percentage

Average Trade value

📱 Alert Settings

Entry Alerts

Long Entry (Buy Signal)

Short Entry (Sell Signal)

Exit Alerts

Long Exit (Take Profit)

Short Exit (Take Profit)

Alert Message Format

Strategy name

Signal type and direction

Current price

Fast SMA value

Slow SMA value

💡 Usage Tips

Consider starting with Long Only mode

Begin with default settings

Keep track of your trades

Review results regularly

Adjust settings as needed

Follow your trading plan

⚠️ Disclaimer

This strategy is for educational and informational purposes only. It is not financial advice. Always:

Conduct your own research

Test thoroughly before live trading

Use proper risk management

Consider your trading goals

Monitor market conditions

Never risk more than you can afford to lose

📋 Release Notes

14 January 2025

Added New Fast & Slow SMA Options:

Fibonacci-based periods: 8, 13, 21, 144, 233, 377

Additional period: 50

Complete Fast SMA options now: 5, 8, 10, 13, 15, 20, 21, 34, 50

Complete Slow SMA options now: 100, 144, 200, 233, 377

Bug Fixes:

Fixed Maximum Drawdown calculation in the performance table

Now using strategy.max_drawdown_percent for accurate DD reporting

Previous version showed incorrect DD values

Performance metrics now accurately reflect trading results

Performance Note:

Strategy tested with Fast/Slow SMA 13/377

Test conducted with 10% equity risk allocation

Daily Timeframe

For Beginners - How to Modify SMA Levels:

Find this line in the code:

fastLength = input.int(title="Fast SMA Length", defval=5, options= )

To add a new Fast SMA period: Add the number to the options list, e.g.,

To remove a Fast SMA period: Remove the number from the options list

For Slow SMA, find:

slowLength = input.int(title="Slow SMA Length", defval=100, options= )

Modify the options list the same way

⚠️ Note: Keep the periods that make sense for your trading timeframe

💡 Tip: Test any new combinations thoroughly before live trading

"Trade with Discipline, Manage Risk, Stay Consistent" - tradeviZion

Recherche dans les scripts pour "profit factor"

MACD Aggressive Scalp SimpleComment on the Script

Purpose and Structure:

The script is a scalping strategy based on the MACD indicator combined with EMA (50) as a trend filter.

It uses the MACD histogram's crossover/crossunder of zero to trigger entries and exits, allowing the trader to capitalize on short-term momentum shifts.

The use of strategy.close ensures that positions are closed when specified conditions are met, although adjustments were made to align with Pine Script version 6.

Strengths:

Simplicity and Clarity: The logic is straightforward and focuses on essential scalping principles (momentum-based entries and exits).

Visual Indicators: The plotted MACD line, signal line, and histogram columns provide clear visual feedback for the strategy's operation.

Trend Confirmation: Incorporating the EMA(50) as a trend filter helps avoid trades that go against the prevailing trend, reducing the likelihood of false signals.

Dynamic Exit Conditions: The conditional logic for closing positions based on weakening momentum (via MACD histogram change) is a good way to protect profits or minimize losses.

Potential Improvements:

Parameter Inputs:

Make the MACD (12, 26, 9) and EMA(50) values adjustable by the user through input statements for better customization during backtesting.

Example:

pine

Copy code

macdFast = input(12, title="MACD Fast Length")

macdSlow = input(26, title="MACD Slow Length")

macdSignal = input(9, title="MACD Signal Line Length")

emaLength = input(50, title="EMA Length")

Stop Loss and Take Profit:

The strategy currently lacks explicit stop-loss or take-profit levels, which are critical in a scalping strategy to manage risk and lock in profits.

ATR-based or fixed-percentage exits could be added for better control.

Position Size and Risk Management:

While the script uses 50% of equity per trade, additional options (e.g., fixed position sizes or risk-adjusted sizes) would be beneficial for flexibility.

Avoid Overlapping Signals:

Add logic to prevent overlapping signals (e.g., opening a new position immediately after closing one on the same bar).

Backtesting Optimization:

Consider adding labels or markers (label.new or plotshape) to visualize entry and exit points on the chart for better debugging and analysis.

The inclusion of performance metrics like max drawdown, Sharpe ratio, or profit factor would help assess the strategy's robustness during backtesting.

Compatibility with Live Trading:

The strategy could be further enhanced with alert conditions using alertcondition to notify the trader of buy/sell signals in real-time.

Golden Cross Strategy with Trend FilterHere's the English translation:

**Entry for Long Position:** Enter a long position only when the 5SMA crosses above the 25SMA and the current price is above the 75SMA.

**Entry for Short Position:** Enter a short position only when the 5SMA crosses below the 25SMA and the current price is below the 75SMA.

**Exit Position:** Hold the long position until a short signal is generated, and hold the short position until a long signal is generated.

By using the 75SMA to confirm the trend direction and taking positions only in alignment with that trend, you can enhance trading accuracy and potentially improve the profit factor.

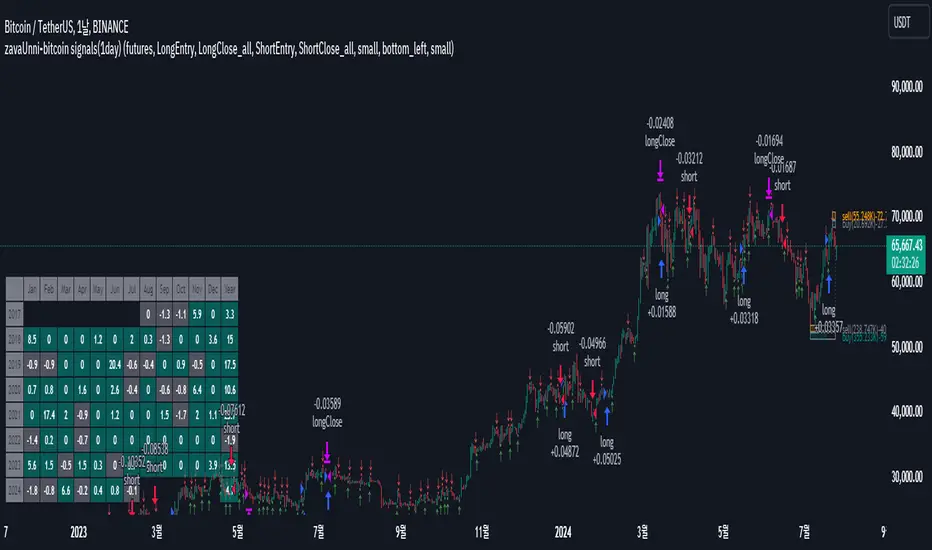

zavaUnni-bitcoin signals(1day)

📌 This strategy predicts price movements based on trading volume and enters positions accordingly. It calculates the expected price increase based on bullish volume and the expected price decrease based on bearish volume to determine the direction of the position.

Top predicted price based on declining bullish volume: top_ifpricebull

Bottom predicted price based on declining bearish volume: top_ifpricebear

Top predicted price based on increasing bullish volume: bot_ifpricebull

Bottom predicted price based on increasing bearish volume: bot_ifpricebear

Using these four values, the strategy calculates the final maxprice and minprice based on volume. If the price settles above the max value, it indicates an upward trend; if it settles below the min value, it indicates a downward trend.

📌 The indicator does not solely rely on the maxprice and minprice conditions. It incorporates complex and sophisticated analysis by considering average volume and candle size.

During a decline, if the average volume and spread of bullish candles exceed those of bearish candles and the price settles above the max value, a long position is entered.

During a rise, if the average volume and spread of bearish candles exceed those of bullish candles and the price settles below the min value, a short position is entered.

Even if the above conditions are met, if the buying pressure significantly outweighs the selling pressure, the position will be closed, but a reverse position will not be entered.

Reviewing historical data shows that while there are instances where the position switches from long to short immediately, there are also cases where the position is closed and re-entered after a few candles.

📌 Trading volume is one of the most traditional yet essential indicators, accurately reflecting price direction. This strategy, which simultaneously predicts fundamental trading volume and price changes, consistently achieves a profit factor above 3.

Characteristics and Historical Data of the Strategy

🔴 Short position entry: April 11, 2022

🟢 Long position entry after closing short: January 11, 2023

⚫ Short position holding period: 270 days

🟢 Long position entry: October 9, 2020

🔵 Long position exit: November 30, 2019

⚫ Long position holding period: 52 days

🟢 Long position entry: November 30, 2019

🔵 Long position exit: February 22, 2021

⚫ Long position holding period: 84 days

Settings Explanation

🛠️ In the input, you can choose between spot and futures. Buy and sell signals are generated in spot trading, while long and short signals are generated in futures trading.

🌈 You can configure the screen view.

Fibonacci Trend

Falling Fibonacci levels from the top: 382 and 618 levels (Red lines)

Rising Fibonacci levels from the bottom: 382 and 618 levels (Green lines)

When the price stays within the 382 and 618 levels of the falling Fibonacci, the background turns red; when it stays within the 382 and 618 levels of the rising Fibonacci, the background turns green.

Real-time Volume Strength of Bullish and Bearish Candles

Red arrow: Appears when the strength of bearish candles increases

Green arrow: Appears when the strength of bullish candles increases

Cumulative Volume of Bullish and Bearish Candles during the Trend

Cumulative data of falling bullish and bearish candles from the top

Cumulative data of rising bullish and bearish candles from the bottom

Profit Table

Provides annual and monthly profit tables.

Setting Options

You can change the options in the attributes to test different configurations.

📌 Trading Data

Although Binance data starts from 2017, limiting the number of trades to 60 as of July 2024, this does not undermine the validity of the strategy. Binance provides reliable volume data, which is crucial for evaluating the strategy's performance. In contrast, exchanges like Bitstamp may have longer trading histories but insufficient volume to properly assess the strategy's actual performance. A volume-based strategy cannot be reliably tested on an exchange with low trading volume. Therefore, despite the limited number of trades on Binance, its reliable volume data justifies its use for this strategy.

► Backtesting Details:

Timeframe: 1D / Bitcoin / TetherUS

Initial Balance: $50,000 (Enter the initial capital you will invest)

Order Size: 10% (Enter the percentage of your account balance you will trade)

Commission: 0.04% (Enter the trading commission)

Slippage: 10 ticks (Enter the slippage you want to test)

When using the strategy:

📢 Timeframe: While the strategy performs well on timeframes lower than daily, it is particularly profitable on the daily timeframe.

📢 Exchange: It is recommended to use Binance due to its reliable volume data.

📢 This strategy is suitable for traders who have the patience to hold positions for extended periods, as it calculates the size of bullish and bearish candles carefully and does not change positions easily.

📢 Spot trading is recommended over futures, and if using futures, leverage should be limited to a maximum of 2x.

RunRox - Backtesting System (SM)RunRox - Backtesting System (SM) is designed for flexible and comprehensive testing of trading strategies, closely integrated with our RunRox - Signals Master indicator. This combination enhances your ability to refine strategies efficiently, providing you with insights to adapt and optimize your trading tactics seamlessly.

The Backtesting System (SM) excels in pinpointing the optimal settings for the RunRox - Signals Master indicator, efficiently highlighting the most effective configurations.

Capabilities of the Backtesting System (SM)

Optimal Settings Determination: Identifies the best configurations for the Signals Master indicator to enhance its effectiveness.

Timeframe-Specific Strategy Testing: Allows strategies to be tested over specific historical time periods to assess their viability.

Customizable Initial Conditions: Enables setting of initial deposit, risk per trade, and commission rates to mirror real-world trading conditions.

Flexible Money Management: Provides options to set take profits and stop losses, optimizing potential returns and risk management.

Intuitive Dashboard: Features a user-friendly dashboard that visually displays all pertinent information, making it easy to analyze and adjust strategies.

Trading Flexibility Across Three Modes:

Dual-Direction Trading: Engage in both buying and selling with this mode. Our dashboard optimizes and identifies the best settings for trading in two directions, streamlining the process to maximize effectiveness for both buy and sell orders.

Buy-Only Mode: Tailored for traders focusing exclusively on purchasing assets. In this mode, our backtester pinpoints the most advantageous sensitivity, speed reaction, and filter settings specifically for buying. Optimal settings in this mode may differ from those used in dual-direction trading, providing a customized approach to single-direction strategies.

Sell-Only Mode: Perfect for strategies primarily based on selling. This setting allows you to discover the ideal configurations for asset sales, which can be particularly useful if you are looking for optimal exit points in long-term transactions or under specific market conditions.

Here's an example of how profits can differ on the same asset when trading using two distinct strategies: exclusively buying or trading in both directions.

Above in the image, you can see how one-directional trading influences the results of backtests on historical data. While this does not guarantee future outcomes, it provides insight into how the strategy's performance can vary with different trading directions.

As you can also see from the image, one-directional trading has affected the optimal combination of settings for Sensitivity, Speed Reaction, and Filters.

Stop Loss and Take Profit

Our backtesting system, as you might have gathered, includes flexible settings for take profits and stop losses. Here are the main features:

Multiple Take Profits: Ability to set from 1 to 4 take profit levels.

Fixed Percentage: Option to assign a fixed percentage for each take profit.

Trade Proportion Fixation: Ability to set a fixed size from the trade for securing profits.

Stop Loss Installation: Option to establish a stop loss.

Break-Even Stop Loss: Ability to move the stop loss to a break-even point upon reaching a specified take profit level.

These settings offer extensive flexibility and can be customized according to your preferences and trading style. They are suitable for both novice and professional traders looking to test their trading strategies on historical data.

As illustrated in the image above, we have implemented money management by setting fixed take profits and stop losses. Utilizing money management has improved indicators such as profit, maximum drawdown, and profit factor, turning even historically unprofitable strategies into profitable ones. Although this does not guarantee future results, it serves as a valuable tool for understanding the effectiveness of money management.

Additionally, as you can see, the optimal settings for Signals Master have been adjusted, highlighting the best configurations for the most favorable outcomes.

Disclaimer:

Historical data is not indicative of future results. All indicators and strategies provided by RunRox are intended for integration with traders' strategies and should be used as tools for analysis rather than standalone solutions. Traders should use their own discretion and understand that all trading involves risk.

Smart Money Concept + Strategy Backtesting Toolkit [Shah]This indicator, primarily designed for strategy backtest. It’s important to emphasize that the orders generated by this indicator are in the form of stop-limit orders .

For Long setup , When lower lows and lower highs form, after price moving up from the last higher high, a “change of character” occurs. Entry will takes place in the golden zone.

This the Long setup:

And this is the Long setup Example on chart:

For Short setup , When higher lows and higher highs form after the price moves down from the last higher low, a “change of character” occurs. Entry will take place within the golden zone.

This the Short setup:

And this is the Short setup Example on chart:

Key Features:

Date Period:

Users can customize the date period during which the strategy is tested, allowing for a more granular analysis of performance over specific timeframes.

DCA Entry:

Entry is based on Fibonacci level between the Lower Low and Higher High pivots for Long deals .

Entry is based on Fibonacci level between the Higher High and Lower Low pivots for Short deals .

Allowing a second entry with a specified position size

Entering at a different price based on a Percent or ATR change.

There is a feature that If the risk-to-reward ratio is below the specified input (rr), the trading deal wont initiate, and the signal alert wont be triggered.

Stop Loss:

Adjustable based on Fibonacci levels , Percent and ATR.

The percent and ATR is calculate from LL pivot point for Long and HH pivot point for short (not Entry price)’

Targets:

Adjustable based on Source, Fibonacci levels , Percent and ATR.

Source indicates the maximum (minimum) value between the open and close of the candle where the Higher High (Lower Low) pivot point was formed for Long (Short) deals.

Percent and ATR calculates from Entry 1 Price

There is a feature that closes the part of the position size at Target 1 based on a percentage, leaving the rest to close at Target 2, entry, exit price, or stop loss.

Plots:

The visual representation of the indicator includes the key plots:

Reset Deal Calculation Fibonacci Level

Alert Fire Fibonacci Level

Entry 1

Entry 2

Entry Average

Stop Loss

Target 1

Target 2

Labels:

Displays informative labels upon trade open and close, providing details about each transaction like gain and equity and etc.

Risk Management:

Allows setting initial capital, risk per trade, and commission for each transaction.

Score Table:

Provides statistical information for Regular deals (refers to deals that closed in Target price or Stop loss price) and Exited deals (representing deals that didn’t touch the stop loss or targets.):

Number of trades

Win rate

Profit factor

Average Risk to Reward ratio

Total Profit and Loss (PnL)

Commission paid

Live equity

It should note that Winrate calculated based on closed deals at target or stop loss. (Exited trades doesn’t into account in calculation of Winrate)

Exit Methods :

The goal is to offer users a diverse set of exits before the price touches the target or stop loss.

1. Pending Entry Time-out

cancel pending entry based on candle counting since alert fired. (before deal started)

2. Break Even

If Target 2 is reached, the stop loss automatically adjusts to the entry price.

3. Active Deal Reverse

If a deal (long or short position) is currently open, and the reverse signal is emitted, the script will close the existing deal.

4. Reverse Deal Exit

If a deal (long or short position) is currently open, and the reverse signal is emitted, the script will automatically close the existing deal.

5. Move Exit

With this method, if Entry 2 is triggered, the deal will be closed when the price touches the Entry price.

6. Candle Counting Exit

This exit type is based on the number of candles since the deal started.

7. Profit Zone Shield Exit

Once a deal enters profit, the Exit level moves to the entry level after reaching a Fibonacci level between TP1 and Entry 1.

Deep Backtesting Table:

It includes:

Time period of the backtest

Pair name and timeframe

Count the long and short trades

Win streak and loss streak

Total deal chances and missed chances

Count the deals goes directly from entry 1 to tp1 and entry 2 to tp1

Count the deals that touched entry 2 and entry 2 filled percent

Count the number of each exit type

Other statistics such as CAGR, Sharpe, Kurtosis, Skewness, and Max Drawdown.

Backtest any Indicator v5Happy Trade,

here you get the opportunity to backtest any of your indicators like a strategy without converting them into a strategy. You can choose to go long or go short and detailed time filters. Further more you can set the take profit and stop loss, initial capital, quantity per trade and set the exchange fees. You get an overall result table and even a detailed, scroll-able table with all trades. In the Image 1 you see the provided info tables about all Trades and the Result Summary. Further more every trade is marked by a background color, Labels and Levels. An opening Label with the trade direction and trade number. A closing Label again with the trade number, the trades profit in % and the total amount of $ after all past trades. A green line for the take profit level and a red line for the stop loss.

Image 1

Example

For this description we choose the Stochastic RSI indicator from TradingView as it is. In Image 2 is shown the performance of it with decent settings.

Timeframe=45, BTCUSD, 2023-08-01 - 2023-10-20

Stoch RSI: k=30, d=40, RSI-length=140, stoch-length=140

Backtest any Indicator: input signal=Stoch RSI, goLong, take profit=9.1%, stop loss=2.5%, start capital=1000$, qty=5%, fee=0.1%, no Session Filter

Image 2

Usage

1) You need to know the name of the boolean (or integer) variable of your indicator which hold the buy condition. Lets say that this boolean variable is called BUY. If this BUY variable is not plotted on the chart you simply add the following code line at the end of your pine script.

For boolean (true/false) BUY variables use this:

plot(BUY ? 1:0,'Your buy condition hold in that variable BUY',display = display.data_window)

And in case your script's BUY variable is an integer or float then use instate the following code line:

plot(BUY ,'Your buy condition hold in that variable BUY',display = display.data_window)

2) Probably the name of this BUY variable in your indicator is not BUY. Simply replace in the code line above the BUY with the name of your script's trade condition variable.

3) Save your changed Indicator script.

4) Then add this 'Backtest any Indicator' script to the chart ...

5) and go to the settings of it. Choose under "Settings -> Buy Signal" your Indicator. So in the example above choose .

The form is usually: ' : BUY'. Then you see something like Image 2

6) Decide which trade direction the BUY signal should trigger. A go Long or a go Short by set the hook or not.

Now you have a backtest of your Indicator without converting it into a strategy. You may change the setting of your Indicator to the best results and setup the following strategy settings like Time- and Session Filter, Stop Loss, Take Profit etc. More of it below in the section Settings Menu.

Appereance

In the Image 2 you see on the right side the List of Trades . To scroll down you go into the settings again and decrease the scroll value. So you can see all trades that have happened before. In case there is an open trade you will find it at the last position of the list.

Every Long trade is green back grounded while Short trades are red.

Every trade begins with a label that show goLong or goShort and its number. And ends with another label again with its number, Profit in % and the resulting total amount of cash.

If activated you further see the Take Profit as a green line and the Stop Loss as a orange line. In the settings you can set their percentage above or below the entry price.

You also see the Result Summary below. Here you find the usual stats of a strategy of all closed trades. The profit after total amount of fees , amount of trades, Profit Factor and the total amount of fees .

Settings Menu

In the settings menu you will find the following high-lighted sections. Most of the settings have a question mark on their right side. Move over it with the cursor to read specific explanation.

Input Signal of your Indicator: Under Buy you set the trade signal of your Indicator. And under Target you set the value when a trade should happen. In the Example with the Stochastic RSI above we used 20. Below you can set the trade direction, let it be go short when hooked or go long when unhooked.

Trade Settings & List of Trades: Take Profit set the target price of any trade. Stop Loss set the price to step out when a trade goes the wrong direction. Check mark the List of Trades to see any single trade with their stats. In case that there are more trades as fits in the list you can scroll down the list by decrease the value Scroll .

Time Filter: You can set a Start Time or deactivate it by leave it unhooked. The same with End Time .

Session Filter: here you can choose to activate it on weekly base. Which days of the week should be trading and those without. And also on daily base from which time on and until trade are possible. Outside of all times and sessions there will be no new trades if activated.

Invest Settings: here you can choose the amount of cash to start with. The Quantity percentage define for every trade how much of the cash should be invested and the Fee percentage which have to be payed every trade. Open position and closing position.

Other Announcements

This Backtest script don't use the strategy functions of TradingView. It is programmed as an indicator. All trades get executed at candle closing. This script use the functionality "Indicator-on-Indicator" from TradingView.

Conclusion

So now it is your turn, take your promising indicators and connect it to that Backtest script. With it you get a fast impression of how successful your indicator will trade. You don't have to relay on coders who maybe add cheating code lines. Further more you can check with the Time Filter under which market condition you indicator perform the best or not so well. Also with the Session Filter you can sort out repeating good market conditions for your indicator. Even you can check with the GoShort XOR GoLong check mark the trade signals of you indicator in opposite trade direction with one click. And compare your indicators under the same conditions and get the results just after 2 clicks. Thanks to the in-build fee setting you get an impression how much a 0.1% fee cost you in total.

Cheers

MMI Auto Backtesting StrategyDescription:

A strategy based on ATR with auto-backtesting capabilities, Take Profit and Stop Loss (either Normal or Trailing). It allows you to select ranges of values and step for each parameter, and backtest the strategy on a multitude of input combinations at once. You can alternatively use a constant value for each parameter. The backtesting results strive to be as close as possible to those given by Tradingview Strategy Tester.

The strategy displays a table with results for different input combinations. This has columns showing current input combination as well as the following stats: Net Profit, Number of trades, % of Profitable trades, Profit Factor, Max Drawdown, Max Runup, Average Trade and Average number of bars in a trade.

You can sort the table by any column (including sorting by multiple columns at the same time) to find, for example, input combination that gives highest Net Profit (or, if sorting by multiple columns, to find input combination with the best balance of Net Profit and % of Profitable trades). You can filter by any column as well (or multiple columns at the same time), using logical expressions like "< value", "> value", "<= value", ">= value". And you can use logical expressions like "< value%" for Net Profit, Max Drawdown, Max Runup and Average trade to filter by percentage value. You will see a "↓" symbol in column's header if that column is sorted from Highest to Lowest, a "↑" symbol if it's sorted from Lowest to Highest and a "𐕢" symbol if that column is being filtered.

The table has customisable styles (like text color, background color of cells, etc.), and can show the total number of backtested combinations with the time taken to test them. You can also change Initial Capital and Position Size (either Contracts, Currency or % of Equity).

Parameters:

The following parameters are located in the "INPUTS (USUAL STRATEGY)" group, and control the behaviour of strategy itself (not the auto-backtesting functionality):

- Period: ATR Length

- Multiplier: ATR Multiplier

- DPO: length of the filtering moving average

- SL: stop loss

- TP: take profit

- Use Stop Loss: enable stop loss

- Stop Loss Mode: stop loss mode (either Normal or Trailing)

- Use Take Profit: enable take profit

- Wicks: use high & low price, or close price

The strategy also has various parameters separated by different groups:

- INPUTS (AUTO-BACKTESTING): has the same parameters as the "INPUTS (USUAL STRATEGY)" group, but controls the input combinations for auto-backtesting; all the numeric parameters have 3 values: F/V (from), T (to) and S (step); if the checkbox to the left of F/V parameter is off, the value of F/V will indicate the constant value used for that parameter (if the checkbox is on, the values will be from F/V to T using step S)

- STRATEGY: contains strategy related parameters like Initial Capital and Position Size

- BACKTESTING: allows you to display either Percentage, Absolute or Both values in the table and has checkboxes that allow you to exclude certain columns from the table

- SORTING: allows you to select sorting mode (Highest to Lowest or vice versa) and has checkboxes in case you want to sort by multiple columns at the same time

- FILTERING: has a text field for each column of the strategy where you can type logical expressions to filter the values

- TABLE: contains styling parameters

Many parameters have the "(i)" description marker, so hover over it to see more details.

Problems:

- The script works best on lower timeframes and continuous markets (trades 24/7), in other cases the backtesting results may vary from those that Tradingview shows

- The script shows closest results when Take Profit and Stop Loss are not used

- Max Runup percentage value is often wrong

Limitations:

- As we are limited by the maximum time a script can be running (which is 20s for Free plan and 40s for Paid plans), we can only backtest several hundreds of combinations within that timeframe (though it depends on the parameters, market and timeframe of the chart you use)

Index Strength Strategy with Signal Using the Index Strength Strategy Indicator for Trading

Introduction:

In this article, we'll explore the Index Strength Strategy Indicator and how it can be used for trading. The Index Strength Strategy Indicator is a technical analysis tool designed to help traders identify trends, determine trend strength, and generate buy and sell signals.

Overview of the Index Strength Strategy Indicator:

The Index Strength Strategy Indicator is based on two moving averages - a fast moving average and a slow moving average - and the Relative Strength Index (RSI). The fast and slow moving averages are used to determine the trend direction, while the RSI is used to calculate the trend strength. The indicator assigns a strength score to the current trend, which is then classified into one of four categories - Very Weak, Weak, Strong, or Very Strong. Traders can use this information to identify the strength of the trend and adjust their trading strategy accordingly.

The indicator also generates buy and sell signals based on a user-defined threshold level. When the strength score crosses above the threshold level, a buy signal is generated, and when the strength score crosses below the threshold level, a sell signal is generated.

Using the Index Strength Strategy Indicator for Trading:

Traders can use the Index Strength Strategy Indicator to identify trends, determine trend strength, and generate buy and sell signals. To use the indicator, traders should first determine the appropriate fast and slow moving average periods and the strength threshold level for their trading style. These input parameters can be adjusted in the indicator's settings.

Once the indicator is added to the chart, traders can use the strength score and trend direction to identify potential trading opportunities. If the trend is classified as Strong or Very Strong, traders may look for opportunities to enter long or short positions in the direction of the trend. If the trend is classified as Very Weak or Weak, traders may look for opportunities to exit or avoid positions.

Traders can also use the buy and sell signals generated by the indicator to enter or exit positions. When a buy signal is generated, traders can enter a long position, and when a sell signal is generated, traders can enter a short position. Traders should set stop-loss and take-profit levels based on their risk management strategy.

Avoiding Mistakes:

To avoid mistakes when using the Index Strength Strategy Indicator, traders should keep the following tips in mind:

Don't rely solely on the indicator - it should be used in conjunction with other technical analysis tools and fundamental analysis.

Use appropriate risk management strategies, including setting stop-loss and take-profit levels.

Adjust the input parameters of the indicator to match your trading style and preferences.

Avoid overtrading and chasing trades - wait for the right opportunities to enter or exit positions.

Trading Strategy Test Results: Time Frame Tested for 15 Mins

To provide an idea of the potential performance of the Index Strength Strategy Indicator, let's look at some recent test results for two popular indices - Bank Nifty and Nifty 50.

From 1-May-2023 to 12-May-2023, using 2 lots of Bank Nifty with the Index Strength Strategy Indicator, a profit of 15,175 was achieved, with a percentage profitable trade rate of 80% and a profit factor of 3.395. The maximum drawdown was 7,000, and the average trade was 3,035.

During the same time period, using 1 lot of Nifty 50 with the Index Strength Strategy Indicator, a profit of 8,187 was achieved

Conclusion:

The Index Strength Strategy Indicator is a useful tool for traders to identify trends, determine trend strength, and generate buy and sell signals. Traders can use the indicator in conjunction with other technical analysis tools and fundamental analysis to make informed trading decisions. By following proper risk management strategies and avoiding common mistakes, traders can use the indicator to improve their trading performance.

Kioseff Trading - AI-Powered Strategy Optimizer Introducing the Kioseff Trading AI-Powered Strategy Optimizer

Optimize and build your trading strategy with ease, no matter your experience level. The Kioseff Trading AI-Powered Strategy Optimizer allows traders to efficiently test and refine strategies with thousands of different profit targets and stop loss settings. Integrated with TradingView's backtester, this tool simplifies strategy optimization, strategy testing, and alert setting, enabling you to enhance your strategy with AI-driven insights.

Key Features:

Comprehensive Testing : Simultaneously test thousands of profit targets and stop losses to fine-tune your strategy.

Dual Strategy Optimization : Adjust and optimize both long and short strategies for balanced performance.

AI Integration : Elevate your strategy with heuristic-based adaptive learning, turning it into a smart, AI-assisted system.

Detailed Analysis : View critical metrics like profit factor, win rate, max drawdown, and equity curve, presented in a strategy script format.

Customizable Alerts : Set alerts for the best version of your strategy.

Flexible Risk Management : Optimize various stop loss types, including profit targets, limit orders, OCO orders, trailing stops, and fixed stops.

Targeted Goals : Choose optimization goals like highest win rate, maximum net profit, or most efficient profit.

Indicator Compatibility : Integrate any strategy/indicator, whether it’s your creation, a favorite author’s, or any public TradingView indicator.

Accessible Design : Navigate a user-friendly interface suitable for traders of all skill levels. No code required.

Precision Lock-In : “Lock” your optimal profit target or stop loss to drill down into precision testing of other variables.

How it works

It's important to remember that merely having the AI-Powered Strategy Optimizer on your chart doesn't automatically provide you with the best strategy. You need to follow the AI's guidance through an iterative process to discover the optimal settings for your strategy.

The Trading Strategy Optimizer is a versatile tool tailored for both non-coding traders and seasoned algorithmic trading professionals. Let's start with no-code-required instructions on how to use the optimizer.

Instructions: How To Optimize Your Strategy Without Code

1. Build your strategy in the settings

The image above shows explanations for each key setting.

Note: This example uses the RSI indicator to initiate a long trade whenever it dips below the 30 mark.

Ensure that the indicator you wish to optimize is already applied to your chart . This enables the Trading Strategy Optimizer to interact with the indicator and finetune profit targets and stop losses effectively.

Because the indicator is plotted on the chart I can access the indicator with the Trading Strategy Optimizer and optimize profit targets and stop losses for it.

2. Leverage AI Recommendations

Optimization Prompt: After you load your strategy, the tool advises you on new TP and SL levels that could be more profitable.

When your strategy is set, the tool gives you tips for where to set your profit goal (TP) and your stop loss to help you optimize your strategy. It'll tell you if there's a better range for these settings based on past results.

Follow Suggestions: Keep updating your TP and SL according to the tool's suggestions until it says "Best Found".

Final Result: The last image shows the best settings found by the indicator.

(Optional Step 3)

3. Lock the profit target or stop loss to further fine tune your strategy

Continue following the AI’s suggestion until “Best Found” is displayed.

Note: you can select lock either your stop loss or profit target for fine tuning. For this demonstration we will lock our profit target.

Code-Required Instructions (Optional)

You can backtest more code-intensive strategies, such as harmonic patterns, traditional chart patterns, candlestick patterns, Elliot wave, etc., by coding the entry condition in your own script and loading it into the Trading Strategy Optimizer. Let's dial in on how to achieve this!

1. You must create an integer variable in your script with an initial value of "0".

2. Define your entry condition in the code. Once complete, assign the value "1" to the variable you created if the entry condition is fulfilled.

3. Plot your variable.

4. Select the plotted variable in the settings for the Trading Strategy Optimizer

The image above shows a coded entry condition for the linear regression channel (which can be any indicator). When price crosses under and closes below the lower line our variable "strategyEntryVariable" is assigned the value "1".

The Trading Strategy Optimizer will treat this change in value from "0" to "1" as an entry signal and enter long/short up to 1000 times at the price where the entry condition was fulfilled.

5. Test Your Strategy

The image above shows the completion of the process! Keep applying the steps we described. Stick with the AI's recommendations until you see “Best Found” show up.

By following these instructions, you can build, test, and optimize almost any trading indicator or strategy!

So, just note that the Trading Strategy Optimizer considers a change in value of a plotted variable from "0" to "1" as an entry signal! So long as you follow this rule you should be able to test and optimize any conceivable, Pine Script compatible strategy!

AI Mode

AI Mode incorporates Heuristic-Based Adaptive Learning to fine-tune trading strategies in a continuous manner. This feature consists of two main components:

Heuristic-Based Decision Making: The algorithm evaluates multiple versions of your strategy using specific metrics such as Profit and Loss (PNL), Win Rate, and Most Efficient Profit. These metrics act as heuristics to assist the algorithm in identifying suitable profit targets and stop losses for trade execution.

Online Learning: The algorithm updates the performance evaluations of each strategy based on incoming market data. This enables the system to adapt to current market conditions.

Incorporating both heuristic-based decision-making and online learning, this feature aims to provide a framework for trading strategy optimization.

Settings

AI Mode Aggressiveness:

Description: The "AI Mode Aggressiveness" setting allows you to fine-tune the AI's trading behavior. This setting ranges from "Low" To "High, with higher aggressiveness indicating a more assertive trading approach.

Functionality: This feature filters trading strategies based on a proprietary evaluation method. A higher setting narrows down the strategies that the AI will consider, leaning towards more aggressive trading. Conversely, a lower setting allows for a more conservative approach by broadening the pool of potential strategies.

Adaptive Learning Aggressiveness:

Description: When Adaptive Learning is enabled, the "Adaptive Learning Aggressiveness" setting controls how dynamically the AI adapts to market conditions using selected performance metrics.

Functionality: This setting impacts the AI's responsiveness to shifts in strategy performance. By adjusting this setting, you can control how quickly the AI moves away from strategies that may have been historically successful but are currently underperforming, towards strategies that are showing current promise.

Additional Settings

Optimization

Trading system optimization is immensely advantageous when executed with prudence.

Technical-oriented, mechanical trading systems work when a valid correlation is methodical to the extent that an objective, precisely-defined ruleset can consistently exploit it. If no such correlation exists, or a technical-oriented system is erroneously designed to exploit an illusory correlation (absent predictive utility), the trading system will fail.

Evaluate results practically and test parameters rigorously after discovery. Simply mining the best-performing parameters and immediately trading them is unlikely a winning strategy. Put as much effort into testing strong-performing parameters and building an accompanying system as you would any other trading strategy. Automated optimization involves curve fitting - it's the responsibility of the trader to validate a replicable sequence or correlation and the trading system that exploits it.

Kioseff Trading - AI-Optimized RSIAI-Optimized RSI

Introducing AI-Optimized RSI: a streamlined solution for traders of any skill level seeking to rapidly test and optimize RSI. Capable of analyzing thousands of strategies, this tool cuts through the complexity to identify the most profitable, reliable, or efficient approaches.

Paired with TradingView's native backtesting capabilities, the AI-Optimized RSI learns from historical performance data. Set up is easy for all skill levels, and it makes fine-tuning trading alerts and RSI straightforward.

Features

Purpose : Uncover optimal RSI settings and entry levels with precision. Say goodbye to random guesses and arbitrary indicator use—this tool provides clear direction based on data.

Target Performance : You set the goal, and AI-RSI seeks it out, whether it's maximizing profits, efficient trading, or achieving the highest win rate.

AI-Powered : With intelligent AI recommendations, the tool dynamically fine-tunes your RSI approach, steering you towards ideal strategy performance.

Rapid Testing : Evaluate thousands of RSI strategies.

Dual Direction : Perfect both long and short RSI strategies with equal finesse.

Deep Insights : Access detailed metrics including profit factor, PnL, win rate, trade counts, and more, all within a comprehensive strategy script.

Instant Alerts : Set alerts and trade.

Full Customization : Test and optimize all RSI settings, including cross levels, profit targets and stop losses.

Simulated Execution : Explore the impact of limit orders and other trade types through simulation.

Integrative Capability : Combine your own custom indicators or others from the TradingView community for a personalized optimization experience.

Flexible Timeframes : Set your optimization and backtesting to any date range.

Key Settings

The image above shows explanations for a list of key settings for the optimizer.

Direction : This setting controls trade direction: Long or Short.

Entry Condition : Define RSI entry: Select whether to trigger trades on RSI crossunders or crossovers.

RSI Lengths Range : Choose the range of RSI periods to test and find the best one.The AI will find the best RSI period for you.

RSI Cross Range : Set the range for RSI levels where crosses trigger trade signals. The AI will find the best level for you.

Combinations : Select how many RSI strategies to compare.

Optimization Type : Choose the goal for optimization and the AI: profit, win rate, or efficiency.

Profit Target : Set your profit target with this setting.

Stop Loss : Decide your maximum allowable loss (stop loss) per trade.

Limit Order : Specify whether to include limit orders in the strategy.

Stop Type : Choose your stop strategy: a fixed stop loss or a trailing stop.

How to: Find the best RSI for trading

It's important to remember that merely having the AI-Optimized RSI on your chart doesn't automatically provide you with the best strategy. You need to follow the AI's guidance through an iterative process to discover the optimal RSI settings and strategy.

1.Starting Your Strategy Setup

Begin by deciding your goals for each trade: your profit target and stop loss. You'll also choose how to manage your stops – whether they stay put (fixed) or move with the price (trailing), and whether you want to exit trades at a specific price (limit orders). Keep the initial settings for RSI lengths and cross ranges at their default to give the tool a broad testing field. The AI's guidance will refine these settings to pinpoint the most effective ones through a process of comprehensive testing.

The image above shows our chart prior to any optimization efforts.

Note: the settings shown above in the key settings section will be used to start our demonstration.

2. Follow AI’s suggestions

Optimization Prompt: After loading your strategy, the indicator will prompt you to change the RSI length range and RSI level range to a better performing range.

Continue changing the RSI length range and RSI level range to match the indicator's suggestions until "Best Found" is displayed!

The image above shows results after we applied the tool’s suggestions. New suggestions have appeared, and we will continue to apply them.

Continue to adjust settings as recommended by the optimizer. If no better options are found, the optimizer will suggest increasing the number of combinations. Repeat this process until the optimizer indicates that the optimal setting has been identified.

Success! With the "Best Found" notification, an optimized RSI is now active. The AI will keep refining the strategy based on ongoing performance, ensuring continuous optimization.

AI Mode

AI Mode incorporates Heuristic-Based Adaptive Learning to fine-tune trading strategies in a continuous manner. This feature consists of two main components:

Heuristic-Based Decision Making: The algorithm evaluates multiple RSI-based trading strategies using specific metrics such as Profit and Loss (PNL), Win Rate, and Most Efficient Profit. These metrics act as heuristics to assist the algorithm in identifying suitable strategies for trade execution.

Online Learning: The algorithm updates the performance evaluations of each strategy based on incoming market data. This enables the system to adapt to current market conditions.

Incorporating both heuristic-based decision-making and online learning, this feature aims to provide a framework for trading strategy optimization.

Settings

AI Mode Aggressiveness:

Description: The "AI Mode Aggressiveness" setting allows you to fine-tune the AI's trading behavior. This setting ranges from “Low” to “High”, with “High” indicating a more assertive trading approach.

Functionality: This feature filters trading strategies based on a proprietary evaluation method. A higher setting narrows down the strategies that the AI will consider, leaning towards more aggressive trading. Conversely, a lower setting allows for a more conservative approach by broadening the pool of potential strategies.

Adaptive Learning Aggressiveness:

Description: When Adaptive Learning is enabled, the "Adaptive Learning Aggressiveness" setting controls how dynamically the AI adapts to market conditions using selected performance metrics.

Functionality: This setting impacts the AI's responsiveness to shifts in strategy performance. By adjusting this setting, you can control how quickly the AI moves away from strategies that may have been historically successful but are currently underperforming, towards strategies that are showing current promise.

Optimization

Trading system optimization is immensely advantageous when executed with prudence.

Technical-oriented, mechanical trading systems work when a valid correlation is methodical to the extent that an objective, precisely-defined ruleset can consistently exploit it. If no such correlation exists, or a technical-oriented system is erroneously designed to exploit an illusory correlation (absent predictive utility), the trading system will fail.

Evaluate results practically and test parameters rigorously after discovery. Simply mining the best-performing parameters and immediately trading them is unlikely a winning strategy. Put as much effort into testing strong-performing parameters and building an accompanying system as you would any other trading strategy. Automated optimization involves curve fitting - it's the responsibility of the trader to validate a replicable sequence or correlation and the trading system that exploits it.

MACD Optimizer Pro [Kioseff Trading]Massive update! This script now includes 12 different moving averages and 30+ built-in technical indicators to enhance your trading strategy optimization! (:

This script (MACD Optimizer Pro) allows the user to optimize and test hundreds of MACD strategies, simultaneously, in under 40 seconds. Of course, theoretically, an unlimited number of trading strategies can be tested with the MACD Optimizer Pro. After the optimization period - the MACD Optimizer Pro will show the most profitable MACD strategy or, should you choose, the highest win-rate MACD strategy or the most-efficient MACD strategy!

Optimization results can be backtested and verified using the native TradingView backtester - which is included in the MACD Optimizer Pro - and made easy to use! This feature makes settings alerts a simple practice!

Features

Test hundreds of MACD strategies, simultaneously, in under 40 seconds.

Optimize long MACD strategies and short MACD strategies.

12 different built-in moving averages included to improve your MACD strategy.

30+ built-in technical indicators to improve your MACD strategy.

Runs as a strategy script - profit factor, PnL , win-rate, number of trades, max drawdown, equity curve and other pertinent statistics shown.

Alerts

Optimize any MACD setting

Profit targets, trailing stops, fixed stop losses, and a binary MACD strategy can all be tested.

Strategies can be optimized for highest win rate, highest net profit, most efficient profit.

Limit orders can be simulated.

External indicators can be used for optimization i.e. your own, custom-built indicator, an indicator from your favorite author, or almost any publicly available

TradingView indicator.

Date range for optimization and backtesting are configurable.

Explanation

The image above shows a list of configurations for the optimizer. You can

You can test hundreds of different MACD settings in under 40 seconds on any timeframe, asset, etc.

The image above shows additional settings to filter the outcome of your optimization testing. Additionally, you can test an unlimited number of profit targets and stop losses!

You can add one of several built-in TradingView indicators to filter trade entries.

The image above shows all built-in moving averages and TradingView indicators that can be incorporated into your MACD strategy.

Additionally, you can add your own, custom indicator to the optimization test, your favorite indicator by your favorite author or almost any publicly available indicator on TradingView.

The image above shows the settings section in which you can implement this feature.

The image above shows an example of the custom indicator feature! In this instance, I am using the public indicator titled "Self-Optimizing" RSI and requiring it to measure below a level prior to entry! Almost any custom indicator, your favorite indicator, etc. is compatible with this feature!

The MACD Optimizer has improved user friendliness over previous versions. The optimizer can be as simple or complex as you'd like - capable of handling both "easy" and "difficult" tasks at your discretion.

Additionally, you can configure the optimizer to prioritize MACD strategies that earn profit most efficiently!

The image above shows this feature in action.

You can also configure the optimizer to prioritize MACD strategies that achieve the highest win rate!

The image above shows this feature in action.

Instructions

The instructions below show a rudimentary approach to using the optimizer.

1. Build your strategy in the settings.

You should also disable the "Run a Backtest" feature to improve load times during optimization.

The image above shows my custom strategy settings.

Now that you've got some data on your chart - you should try "Freezing" the "Smoothing" setting for MACD . When doing this, the optimizer will test hundreds of MACD settings with a fixed "Smoothing" setting. Try using the best "Smoothing" setting you were able to find for your initial testing.

2. Take the best "Smoothing" setting and test various MACD and Signal Lengths.

The image above shows me configuring the MACD Optimizer to test different MACD line lengths and Signal line lengths with a fixed "smoothing" setting.

From the results, we can see that there are better MACD settings than what was shown in our initial test!

With this information we can execute a TradingView backtest.

3. Execute a TradingView Backtest.

You must enable the "Run a Backtest" feature to perform a TradingView backtest. Additionally, it's advised to enable the "STOP OPTIMIZATION" feature when performing a TradingView backtest. Enabling this feature will improve load times for the backtest to only a few seconds (since the optimizer won't look for the best setting when this feature is enabled).

The image above shows completion of the process!

From here, you can perform further testing, set alerts, etc.

Backtest Settings Shown

Initial Capital: The initial capital used for the shown backtests is $3,500 USD. Set the initial capital to replicate your true starting capital (: PnL for the MACD strategies (listed in table) is calculated using a starting capital of $10,000 USD.

Slippage: The slippage settings for the displayed backtest was set to 2 ticks.

Commission: Commission was adjusted to 0.1%.

Verify Price for Limit Orders was set to 2 ticks.

Optimization

Trading system optimization is immensely advantageous when executed with prudence.

Technical-oriented, mechanical trading systems work when a valid correlation is methodical to the extent that an objective, precisely-defined ruleset can consistently exploit it. If no such correlation exists, or a technical-oriented system is erroneously designed to exploit an illusory correlation (absent predictive utility), the trading system will fail.

Evaluate results practically and test parameters rigorously after discovery. Simply mining the best-performing parameters and immediately trading them is unlikely a winning strategy. Put as much effort into testing strong-performing parameters and building an accompanying system as you would any other trading strategy. Automated optimization involves curve fitting - it's the responsibility of the trader to validate a replicable sequence or correlation and the trading system that exploits it.

Thanks for checking this out!

[SPOILED]SuperTrench - ETH Super ScalperHi Traders,

I'm republishing this script as I finally polished it to perfection IMO. The script uses 5 coding sections: entry, trend filter, pivot filter, take profit, and stop loss. The script mainly uses trailing as take profit; this is probably the easiest way to make a profitable scalper strategy.

Backtest capital is set to 1000 USDT, 35% equity, 0.04% commission, limited backtest date from Jan 2022 to now, backtested on ETH/USDT prep contracts 15m timeframe, result as shown below.

It looks unreal right? Hell no, I actually tested this strategy on Binance from Dec 06 to Dec 10. I got 8.29% return with 4x leverage, 50% equity setup; 75% win rate,1.58 profit factor, with 4.3% max drawdown, it is amazingly close to the backtest result.

User Manual

Entry >>> Stoch RSI:

I added 5 MA types to the Stoch RSI which is HMA/VWMA/WMA/EMA/SMA, HMA with Length setting of 5, 8 seems to be most efficient, VWMA and WMA with 8, 13 will generate less entry signals but with less entry risks.

Entry >>> R Style:

It based on price action, with candlestick makes a U turn, after 2nd candlestick confirmed, it generates entry signal, this will give you some extra entries, better leave it enabled.

Entry >>> Price Step:

This probably is the core feature of this strategy; also my secret ingredient to making this strategy this efficient. It is recommended to enable step 1-5, more steps basically means more entries, but they are not necessarily profitable.

Trend Filter >>> Price Step:

I couldn't tell you much details about how this indicator works, but it is a reliable indicator, based on price action, and I got some ideas from Demark9 indicator. The bigger the level, the stronger the filter is, please note that if 'Price Step Entries' less than Price Step Trend, entries will be ignored.

Pivot Filter >>> RSI Pivot & Pinbar Pivot:

RSI Pivot detects if the RSI signal line making U turn in certain condition, Pinbar detection combines R Style entry when price action U turn took place, these 2 pivot filter will close the trade once it is counter trend, so it better enable and leave it as is.

Trend Filter >>> Trend Magic:

Trend Magic uses CCI and ATR to calculate trend status, green means uptrend, red means downtrend, pretty straight forward, the best value for this indicator would be, 21, 34, 55, 89.

Trend Filter >>> Alpha:

This filter combines R style pivot, price step, EMA all together to detects consolidation area, because EMA was involved, so the best look back period would be around 15-35, it is best to use default value IMO, in another hands, if you need stronger filter, feel free to use 10, 18, 20, 25, 30, 35, make sure look back period should increase or decrease by 5 every time.

Take Profit and Stop Loss:

The default value for tp is set to 0.4%, but I also give you option to switch to ATR TP; you can adjust in the ATR multiplier, default ATR trailing stop loss uses 1 ATR, but you can adjust it for better drawdown tolerance. Fixed ATR SL is also given when fixed ATR is enabled. There will be a failsafe SL default set to 1% if price moves counter direction of opened position, it will close trade no matter what happens.

Enjoy :)

Strategy Myth-Busting #20 - HalfTrend+HullButterfly - [MYN]#20 on the Myth-Busting bench, we are automating the " I Found Super Easy 1 Minute Scalping System And Backtest It 100 Times " strategy from " Jessy Trading " who claims 30.58% net profit over 100 trades in a couple of weeks with a 51% win rate and profit factor of 1.56 on EURUSD .

This one surprised us quite a bit. Despite the title of this strategy indicating this is on the 1 min timeframe, the author demonstrates the backtesting manually on the 5 minute timeframe. Given the simplicity of this strategy only incorporating a couple of indicators, it's robustness being able to be profitable in both low and high timeframes and on multiple symbols was quite refreshing.

The 3 settings which we need to pay most attention to here is the Hull Butterfly length, HalfTrend amplitude and the Max Number Of Bars Between Hull and HalfTrend Trigger. Depending on the timeframe and symbol, these settings greatly impact the performance outcomes of the strategy. I've listed a couple of these below.

And as always, If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 3 open-source public indicators:

Hull Butterfly Oscillator by LuxAlgo

HalfTrend by Everget

Trading Rules

5 min candles but higher / lower candles work too.

Stop loss at swing high/low

Take Profit 1.5x the risk

Long

Hull Butterfly gives us green column, Wait for HalfTrend to present an up arrow and enter trade.

Short

Hull Butterfly gives us a red column , Wait for HalfTrend to present a down arrow and enter trade.

Alternative Trading Settings for different time frames

1 Minute Timeframe

Move the Hull Butterfly length from the default 11 to 9

Move the HalfTrend Amplitude from the default 2 to 1

Enabling ADX Filter with a 25 threshold

2 Hour Timeframe

Move the HalfTrend Amplitude from the default 2 to 1

Laddered Take Profits from 14.5% to 19% with an 8% SL

LuxAlgo - Backtester (S&O)The S&O Backtester is an innovative strategy script that encompasses features + optimization methods from our Signals & Overlays™ toolkit and combines them into one easy-to-use script for backtesting the most detailed trading strategies possible.

Our Signals & Overlays™ toolkit is notorious for its signal optimization methods such as the 'Optimal Sensitivity' displayed in its dashboard which provides optimization backtesting of the Sensitivity parameter for the Confirmation & Contrarian Signals.

This strategy script allows even more detailed & precise backtests than anything available previously in the Signals & Overlays™ toolkit; including External Source inputs allowing users to use any indicator including our other paid toolkits for take profit & stop loss customization to develop strategies, along with 10+ pre-built filters directly Signals & Overlays™' features.

🔶 Features

Full Sensitivity optimization within the dashboard to find the Best Win rates or Best Profits.

Counter Trade Mode to reverse signals in undesirable market conditions (may introduce higher drawdowns)

Built-in filters for Confirmation Signals w/ Indicator Overlays from Signals & Overlays™.

Built-in Confirmation exit points are available within the settings & on by default.

External Source Input to filter signals or set custom Take Profits & Stop Losses.

Optimization Matrix dashboard option showing all possible permutations of Sensitivity.

Option to Maximize for Winrate or Best Profit.

🔶 Settings

Sensitivity signal optimizations for the Confirmation Signals algorithm

Buy & Sell conditions filters with Indicator Overlays & External Source

Take Profit exit signals option

External Source for Take Profit & Stop Loss

Sensitivity ranges

Backtest window default at 2,000 bars

External source

Dashboard locations

🔶 Usage

Backtests are not necessarily indicative of future results, although a trader may want to use a strategy script to have a deeper understanding of how their strategy responds to varying market conditions, or to use as a tool for identifying possible flaws in a strategy that could potentially be indicative of good or bad performance in the future.

A strategy script can also be useful in terms of it's ability to generate more complete & configurable alerts, giving users the option to integrate with external processes.

In the chart below we are using default settings and built-in optimization parameters to generate the highest win rate.

Results like the above will vary & finding a strategy with a high win rate does not necessarily mean it will persist into the future, however, some indications of a well-optimized strategy are:

A high number of closed trades (100+) with a consistently green equity curve

An equity curve that outperforms buy & hold

A low % max drawdown compared to the Net Profit %.

Profit factor around 1.5 or above

In the chart below we are using the Trend Catcher feature from Signals & Overlays™ as a filter for standard Confirmation Signals + exits on a higher timeframe.

By filtering bullish signals only when the Trend Catcher is bullish, as well as bearish signals for when the Trend Catcher is bearish, we have a highly profitable strategy created directly from our flagship features.

While the Signals & Overlays features being used as built-in filters can generate interesting backtests, the provided External Sources can allow for even more creativity when creating strategies. This feature allows you to use many indicators from TradingView as filters or to trigger take-profit/stop-loss events, even if they aren't from LuxAlgo.

The chart below shows the HyperWave Oscillator from our Oscillator Matrix™ being used for take-profit exit conditions, exiting a long position on a profit when crossing 80, and exiting a short position when crossing 20.

🔶 Counter Trade Mode

Our thesis has always firmly remained to use Confirmation Signals within Signals & Overlays™ as a supportive tool to find trends & use as extra confirmation within strategies.

We included the counter-trade mode as a logical way to use the Confirmation signals as direct entries for longs & shorts within more contrarian trading strategies. Many traders can relate to using a trend-following indicator and having the market not respect its conditions for entries.

This mode directly benefits a trader who is aware that market conditions are generally not-so-perfect trends all the time. Acknowledging this, allows the user to use this to their advantage by introducing countertrend following conditions as direct entries, which tend to perform very well in ranging markets.

The big downfall of using counter-trade mode is the potential for very large max-drawdowns during trending market conditions. We suggest for making a strategy to consider introducing stop-loss conditions that can efficiently minimize max-drawdowns during the process of backtesting your creations.

Sensitivity Optimization

Within the Signals & Overlays™ toolkit, we allow users to adjust the Confirmation Signals with a Sensitivity parameter.

We believe the Sensitivity paramter is the most realistic way to generate the most actionable Confirmation Signals that can navigate various market conditions, and the Confirmation Signals algorithm was designed specifically with this in mind.

This script takes this parameter and backtests it internally to generate the most profitable value to display on the dashboard located in the top right of the chart, as well as an optimization table if users enable it to visualize it's backtesting.

In the image below, we can see the optimization table showing permutations of settings within the user-selected Sensitivity range.

The suggested best setting is given at the current time for the backtesting window that's customizable within the indicator. Optimized settings for technical indicators are not indicative of future results and the best settings are highly likely / guaranteed to change over time.

Optimizing signal settings has become a popular activity amongst technical analysts, however, the real-time beneficial applications of optimizing settings are limited & best described as complicated (even with forward testing).

🔶 Strategy Properties (Important)

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access on our website.

Trend Follower Intraday [ Adjustable TF ]Trend Follower Intraday for 3 minute Time-Frame (Adjustable) , that has the time condition for Indian Markets as well.

Unlike the Free Scripts - Risk Management , Position Sizing , Partial Exit etc. are also included .

Send us a Message to know more about the strategy.

// ══════════════════════════════════════════════════════════════════════════ //

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) EMA1 crosses above EMA2 , is a Long condition .

2) EMA1 crosses below EMA2 , is a Short condition .

3) Green Section indicates Long position.

4) Red Section indicates Short position.

5) Allowed hours specifies the trade entry timing.

6) ATR STOP is the stop-loss value on chart , can be adjusted in INPUTS.

7) Target 1 is the 1st target value on chart , can be adjusted in INPUTS.

8) RISK is Maximum Risk per trade for the intraday trade can be changed .

9) Total Capital used can be adjusted under INPUTS.

10) ATR TRAIL is used for trailing after entry, as mentioned in the inputs below.

11) Check trades under the list of trades .

12) Trade only in liquid stocks .

13) Risk only 1-5% of total capital.

14) Inputs can be changed for better back-test results, but also manually check the trades before setting alerts

15) SQUARE OFF TIME - As you change the time frame , also change the square-off time to the candle's closing time.

Eg: For 3min Time-frame , Hour = 2Hrs | Minute = 57min

16) Strategy stops for the day if you have a loss .

17) COMMISSION value is set to 20Rs and SLIPPAGE value is set to 2 . Go to properties to change it .

*The input values and the results are mentioned under "BACKTEST RESULTS" below*

// ══════════════════════════════ //

// ————————> RISK MANAGEMENT <——————— //

// ══════════════════════════════ //

Risk management is done based on max loss per trade and can be adjusted in the INPUTS.

// ═══════════════════════════ //

// ————————> POSITION SIZE <——————— //

// ═══════════════════════════ //

Quantity of each trade is different based on the loss

// ═════════════════════════ //

// ————————> PROPERTIES <——————— //

// ═════════════════════════ //

COMMISSION , SLIPPAGE ,RECALCULATE is already mentioned in the code.

COMMISSION can be charges , based on the broker charges.

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the INPUT.

The Indian Markets open at 9:15am and closes at 3:30pm.

The 'Allowed hours' under Inputs specifies the time at which Entries should happen .

"Close All" function closes all the trades before 3pm , at the open of the next candle.

To change the time to close all trades , check INPUT.

All open trades get closed by 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 123 CLOSED TRADES ) <————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better Back-Test results.

The strategy applied to NSE:JSWENERGY (3 min Time-Frame and with a capital of 3,00,000 ) gives us 81% profitability , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.957 ,net Profit of 43,000Rs .

Sharpe Ratio = 0.745

Sortino Ratio = 2.091

No strategy in the world promises 100% profits in all market conditions , so always define your risk before trading.

Also check Back-Test results manually ,before setting Alerts

The Graph has a Linear Curve with Consistent Profits.

The INPUTS are as follows,

1) EMA1 ————————————————> 38

2) EMA2 ————————————————> 118

3) ALLOWED HRS ———————————> 9:35 TO 14:30

4) ATR STOP ——————————————> 3.2

5) RISK ——————————————————> 3000

6) ATR TRAIL ———————————————> 2.6

7) TARGET 1 ————————————————> 2.4

8) MAX POSITION VALUE ——————————> 3,00,000

8) MAX DRAWDOWN —————————————> 9,000

8) SQUARE-OFF ————————————————> 14:57

NSE:JSWENERGY

Apply it to your charts Now !

NSE:JSWENERGY

Send us a message for FREE TRIALS | Instant Access

Thank You ☺

SUPPORT RESISTANCE STRATEGY [5MIN TF]A SUPPORT RESISTANCE BREAKOUT STRATEGY for 5 minute Time-Frame , that has the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above Resistance Level ,indicated by Red Line, is a Long condition.

2) Price crosses below Support Level ,indicated by Green Line , is a Short condition.

3) Candle high crosses above ema1, is a part of the Long condition .

4) Candle low crosses below ema1, is a part of the Short condition .

5) Volume Threshold is an added confirmation for long/short positions.

6) Maximum Risk per trade for the intraday trade can be changed .

7) Default qty size is set to 50 contracts , which can be changed under settings → properties → order size.

8) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

→ L_Bars ———————————> Length of Resistance / Support Levels.

→ R_Bars ———————————> Length of Resistance / Support Levels.

→ Volume Break ———————> Volume Breakout from range to confirm Long/Short position.

→ Price Cross Ema —————> Added condition as explained above (3) and (4).

→ ATR LONG —————————> ATR stoploss trail for Long positions.

→ ATR SHORT ————————> ATR stoploss trail for Short positions.